by Phil Larson

On December 24th, the IRS, DOL, and HHS published proposed regulations dealing with the kinds of plans that may be covered under ERISA, the CODE, and the PHSA. This includes rules that are part of the Market Reform rules of the Affordable Care Act (ACA).

The proposed rules attempt to clarify three new kinds of plans that are considered excepted benefits and therefore not subject to some of the plan compliance rules identified above. [For additional discussion on excepted benefit plans, please see separate blog on this topic dated 8/13/13.]

The proposed regulations generally clarify when the following programs will qualify as an excepted benefit.

LIMITED SCOPE DENTAL OR VISION

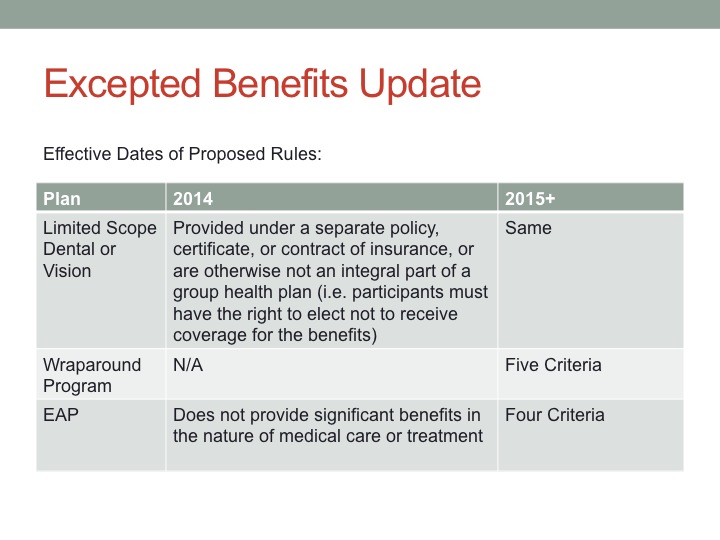

First, the rules clarify that to minimize ACA concerns and to level the playing field for insured vs self-insured programs, they are eliminating the requirement that that participants pay an additional premium or contribution for limited-scope vision or dental benefits to qualify as benefits that are not an integral part of a plan. This makes it easier for some dental and vision programs to qualify as excepted benefits.

LIMITED WRAPAROUND PROGRAMS

Second, starting in 2015, the rules will treat certain wraparound coverage provided under a group health plan as excepted benefits when it is offered to individuals who could receive such benefits through their group health plan if they could afford the premiums, but who do not enroll in the employer-sponsored plan because the premium is unaffordable under the law. These plans must meet FIVE criteria in order to be considered excepted benefits including what it can wraparound, what it covers, how it coordinates with a primary health plan, limits on the amounts of coverage, and certain nondiscrimination requirements.

An example of a wraparound plan may be one that provides some benefits in addition to essential health benefits or one that reimburses the cost of out-of-network providers under individual health insurance. The preamble to the rules indicates this "exception" may allow an employer to provide additional coverage to employees with exchange coverage.

LIMITED EMPLOYEE ASSISTANCE PLANS (EAPs)

Guidance in September 2013 already hinted the departments intend to provide guidance that EAPs will be excepted benefits. The prior guidance provided transition relief, stating, “[u]ntil rulemaking is finalized, through at least 2014, the Departments will consider an employee assistance program or EAP to constitute excepted benefits only if the employee assistance program or EAP does not provide significant benefits in the nature of medical care or treatment. Starting in 2015, EAPs will continue to be excepted benefits if they meet FOUR criteria including the requirement that it not provide significant benefits, it not coordinate with other group health plans, there is no premium charged, and no cost sharing.

To view the guidance, click here.

It is important to note that offering excepted benefits may not require some of the complicated compliance obligations associated with an employee benefits plan (like part 7 of ERISA), but will also not satisfy the employer mandate, the individual mandate, or impact subsidy eligibility for individuals. To understand the effective dates of the proposed rules by plan, please see below.

If you need help understanding which plans are excluded from various compliance requirements including the ACA, please contact Kinney & Larson.

On December 24th, the IRS, DOL, and HHS published proposed regulations dealing with the kinds of plans that may be covered under ERISA, the CODE, and the PHSA. This includes rules that are part of the Market Reform rules of the Affordable Care Act (ACA).

The proposed rules attempt to clarify three new kinds of plans that are considered excepted benefits and therefore not subject to some of the plan compliance rules identified above. [For additional discussion on excepted benefit plans, please see separate blog on this topic dated 8/13/13.]

The proposed regulations generally clarify when the following programs will qualify as an excepted benefit.

LIMITED SCOPE DENTAL OR VISION

First, the rules clarify that to minimize ACA concerns and to level the playing field for insured vs self-insured programs, they are eliminating the requirement that that participants pay an additional premium or contribution for limited-scope vision or dental benefits to qualify as benefits that are not an integral part of a plan. This makes it easier for some dental and vision programs to qualify as excepted benefits.

LIMITED WRAPAROUND PROGRAMS

Second, starting in 2015, the rules will treat certain wraparound coverage provided under a group health plan as excepted benefits when it is offered to individuals who could receive such benefits through their group health plan if they could afford the premiums, but who do not enroll in the employer-sponsored plan because the premium is unaffordable under the law. These plans must meet FIVE criteria in order to be considered excepted benefits including what it can wraparound, what it covers, how it coordinates with a primary health plan, limits on the amounts of coverage, and certain nondiscrimination requirements.

An example of a wraparound plan may be one that provides some benefits in addition to essential health benefits or one that reimburses the cost of out-of-network providers under individual health insurance. The preamble to the rules indicates this "exception" may allow an employer to provide additional coverage to employees with exchange coverage.

LIMITED EMPLOYEE ASSISTANCE PLANS (EAPs)

Guidance in September 2013 already hinted the departments intend to provide guidance that EAPs will be excepted benefits. The prior guidance provided transition relief, stating, “[u]ntil rulemaking is finalized, through at least 2014, the Departments will consider an employee assistance program or EAP to constitute excepted benefits only if the employee assistance program or EAP does not provide significant benefits in the nature of medical care or treatment. Starting in 2015, EAPs will continue to be excepted benefits if they meet FOUR criteria including the requirement that it not provide significant benefits, it not coordinate with other group health plans, there is no premium charged, and no cost sharing.

To view the guidance, click here.

It is important to note that offering excepted benefits may not require some of the complicated compliance obligations associated with an employee benefits plan (like part 7 of ERISA), but will also not satisfy the employer mandate, the individual mandate, or impact subsidy eligibility for individuals. To understand the effective dates of the proposed rules by plan, please see below.

If you need help understanding which plans are excluded from various compliance requirements including the ACA, please contact Kinney & Larson.